From FY 2024-25, the new tax regime became the default — meaning if you don't explicitly declare your choice to your DDO, your TDS is computed under the new regime. For many government employees, this default costs money. Here's how to figure out which regime actually saves you more.

Key change for FY 2025-26: The new regime rebate limit was raised to Rs. 12 lakh under Budget 2025 — meaning those earning up to Rs. 12 lakh pay zero tax under the new regime. This significantly shifted the break-even point. Government employees need to recalculate, not rely on last year's comparison.

New Regime: What You Get and What You Lose

The new regime offers lower slab rates — and from FY 2025-26, zero tax up to Rs. 12 lakh annual income (via Section 87A rebate). The trade-off: you lose most major deductions and exemptions, including:

- HRA exemption under Section 10(13A)

- Section 80C deductions (ELSS, PPF, NSC, LIC premium, NPS employee contribution)

- Section 80D (health insurance premium)

- Leave Travel Allowance exemption

- Standard deduction is retained at Rs. 75,000 (revised upward from Rs. 50,000)

- NPS employer contribution deduction under 80CCD(2) is still allowed

Old Regime: What You Keep

Under the old regime, the tax slabs are higher — but you retain all deductions. For a government employee, the major ones are:

- HRA exemption — potentially Rs. 1–2 lakh/year depending on rent and city

- Section 80C — up to Rs. 1.5 lakh (GPF contribution, NPS employee share, LIC, NSC)

- Section 80CCD(1B) — additional Rs. 50,000 for voluntary NPS contribution

- Standard deduction of Rs. 50,000

- Section 80D — up to Rs. 25,000 for health insurance (Rs. 50,000 for senior citizens)

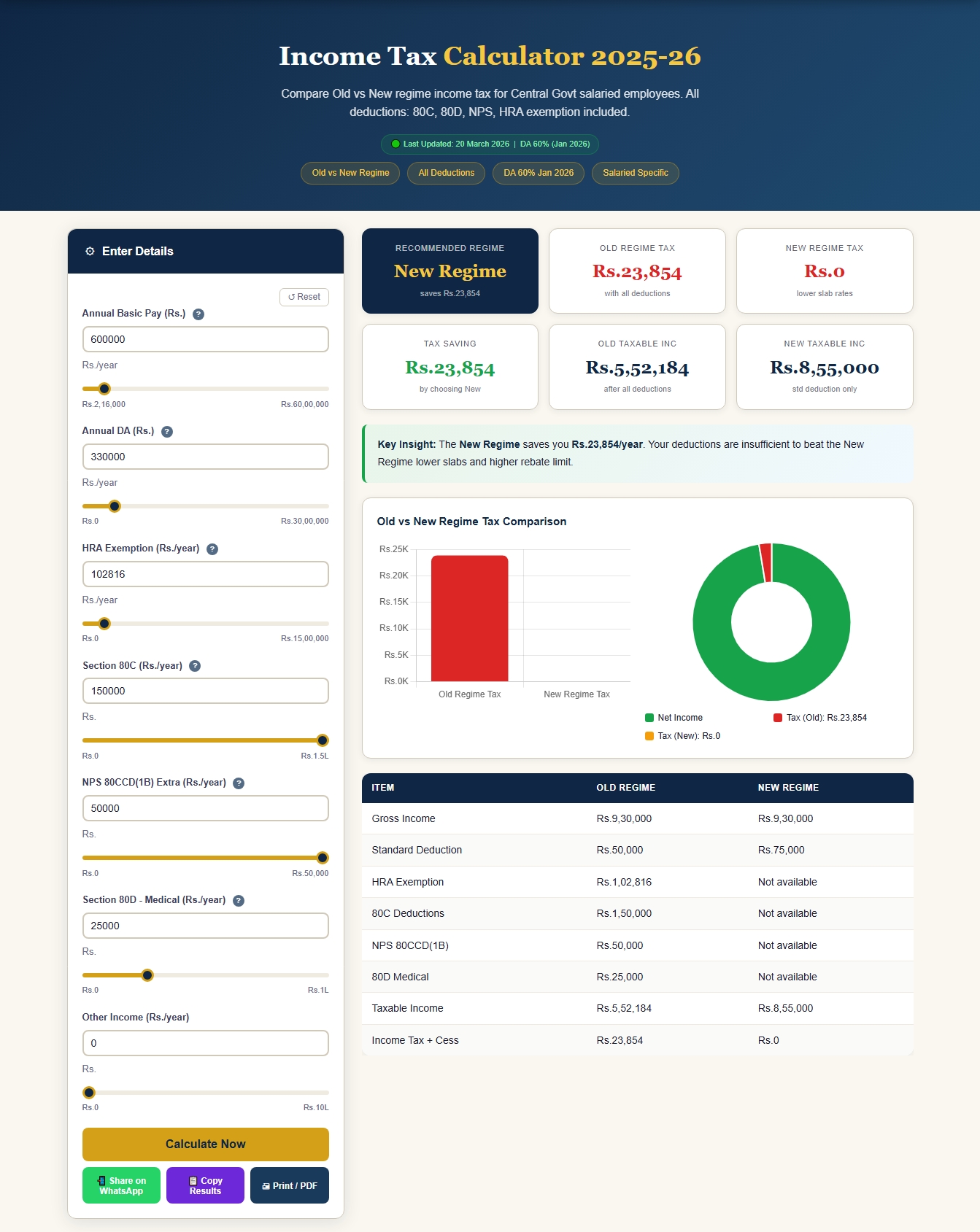

The Break-Even Calculation

The question is simple: do your total old-regime deductions reduce your taxable income enough to make the higher old-regime slab rates worthwhile? Let's compare two real cases.

Case 1: Level 7 Employee, Y-Class City, Paying Rent

| Item | Old Regime (Rs.) | New Regime (Rs.) |

|---|---|---|

| Gross Salary (annual) | 10,59,936 | 10,59,936 |

| Standard Deduction | –50,000 | –75,000 |

| HRA Exemption | –72,000 | Not allowed |

| 80C (NPS + GPF) | –1,50,000 | Not allowed |

| 80CCD(2) Employer NPS | –89,208 | –89,208 |

| Taxable Income | ~6,98,728 | ~8,95,728 |

| Estimated Tax + Cess | ~Rs. 37,500 | ~Rs. 42,000 |

In this case, the old regime saves approximately Rs. 4,500/year. Not dramatic — but real. The bigger the HRA exemption and 80C contribution, the more the old regime wins.

Case 2: Level 12 Employee, Z-Class City, Own House

A higher-level employee posted in a Z-class city, living in their own house, receives 9% HRA (taxable, since no rent is paid) and has lower HRA exemption. Here, the new regime's lower rates and Rs. 12 lakh rebate structure often win — especially since 80C is already saturated and HRA exemption is zero.

💼 Compare Both Tax Regimes

Enter your gross salary, HRA, rent, and deductions to see your exact tax liability under both regimes side by side.

When New Regime Wins for Government Employees

The new regime is better when:

- Annual income is close to or below Rs. 12 lakh (zero tax under new regime)

- You live in government quarters (no HRA exemption possible)

- You are posted in a Z-class city with low HRA and pay no rent

- You have minimal 80C investments (no PPF, ELSS, or LIC)

- You are in the early years of service with lower Basic Pay

When Old Regime Wins

The old regime is better when:

- You pay significant rent in an X or Y-class city (HRA exemption is large)

- You have maximised 80C at Rs. 1.5 lakh plus additional 80CCD(1B)

- Annual income is between Rs. 12–20 lakh range with substantial deductions

- You have a home loan with interest deduction under Section 24

The Regime Choice Deadline

You must declare your tax regime choice to your DDO at the beginning of the financial year (April). Once declared, you cannot change it mid-year for TDS purposes — though you can switch when filing your actual ITR. If you don't declare, the new regime applies by default. Revisit this decision every April — your personal situation changes with promotions, city transfers, and family circumstances.

Frequently Asked Questions

Can I switch between old and new regime every year?

Salaried employees can switch once per year — at the time of filing ITR. However, for TDS purposes during the year, you're locked into whichever choice you declared to your DDO in April. If you chose new regime for TDS but old regime is better, you'll get a refund when you file ITR.

Is NPS employer contribution (14%) exempt in both regimes?

Yes. The employer's (government's) 14% NPS contribution is exempt under Section 80CCD(2) in both old and new regimes, up to 14% of Basic + DA. This is one of the most valuable tax benefits that survives the switch to the new regime — and it's often overlooked.