This is one of the most debated topics in government service — not just in official circles, but in canteens, training halls, and WhatsApp groups. Pre-2004 employees who retained GPF will retire with a defined pension. Post-2004 employees under NPS will retire with a corpus they must manage. Who ends up better off? The answer is more nuanced — and data-dependent — than most discussions acknowledge.

Who this applies to: All Central Govt employees recruited before January 1, 2004 are under the Old Pension Scheme (OPS) with GPF. Those recruited on or after that date are under NPS. There is currently no provision to switch between the two for Central Govt employees (unlike some State Governments).

What GPF Actually Gives You

The General Provident Fund is a defined-contribution savings vehicle for pre-2004 employees. You contribute a minimum of 6% of Basic Pay (most contribute 10–12%), and the government credits interest at a notified rate — currently 7.1% per annum for 2025-26, compounded annually. At retirement, you receive the entire corpus as a lump sum — tax-free if you've been in service for 5+ years.

But GPF alone doesn't fund retirement. The real retirement security for pre-2004 employees is the Defined Benefit Pension — 50% of last drawn Basic Pay (or average of last 10 months, whichever is higher) as a monthly pension for life, with survivor benefits. That pension is the guaranteed income floor, not GPF.

What NPS Actually Gives You

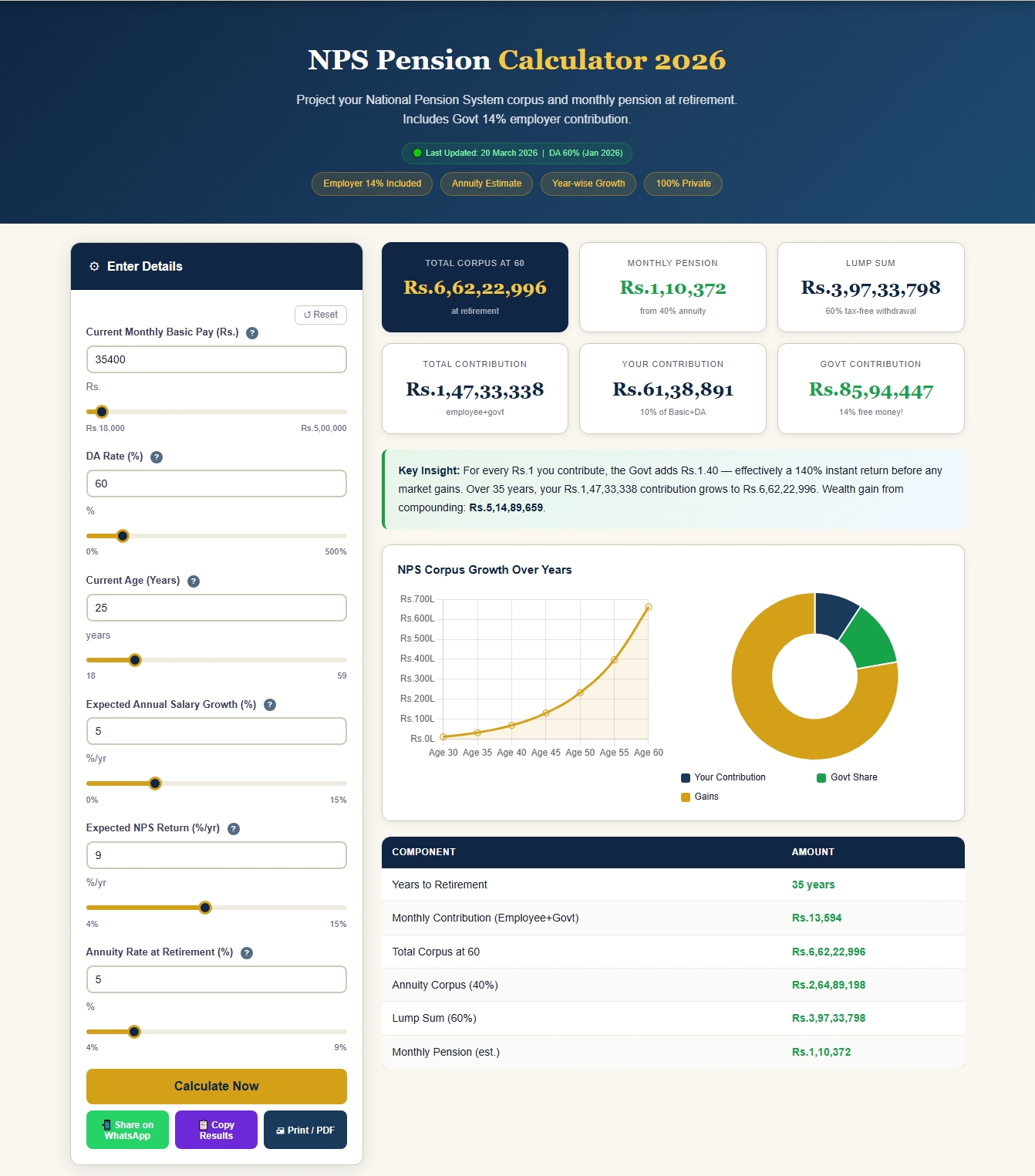

Under NPS, both you (10% of Basic + DA) and the government (14% of Basic + DA) contribute to your Tier-I account every month. These funds are invested in market-linked instruments — Equity (E), Government Securities (G), and Corporate Bonds (C) — based on your scheme choice. At retirement (age 60), you must use at least 40% of the corpus to purchase an annuity (monthly pension), and you can withdraw the remaining 60% tax-free.

The government's 14% contribution is the key differentiator — it doesn't appear on your salary slip, but it's real money compounding in your account every month.

The Corpus Comparison: Running the Numbers

Let's compare two employees, both joining at age 25 with Basic Pay Rs. 35,400 (Level 6), retiring at age 60. GPF employee contributes 10% of Basic, NPS employee gets 10% + 14% = 24% of Basic + DA combined.

| Parameter | GPF Employee | NPS Employee |

|---|---|---|

| Monthly contribution rate | 10% of Basic | 24% of Basic+DA (combined) |

| Approx. starting contribution | Rs. 3,540/month | Rs. 8,496/month |

| Return assumption | 7.1% p.a. (fixed) | 9–10% p.a. (market estimate) |

| Corpus at retirement (35 yrs) | ~Rs. 62 lakh | ~Rs. 3.2–3.8 crore |

| Monthly pension | ~Rs. 50,000+ (guaranteed) | ~Rs. 80,000–1 lakh (annuity, not guaranteed) |

On pure corpus math, NPS wins substantially — driven largely by the government's 14% contribution and the power of equity returns over 35 years. But NPS pension is not guaranteed: if markets underperform or if you're unlucky with annuity rates at retirement, the actual pension could be lower.

🏢 Project Your NPS Corpus

Enter your Basic Pay, years of service remaining, and expected return to see your projected retirement corpus and monthly pension.

The GPF Interest Rate Risk

GPF interest rates are notified quarterly by the government and have been gradually declining over the past decade — from 8.7% in 2016 to 7.1% today. There is no guarantee the rate won't fall further. If GPF rates drop to 6% or below, the corpus advantage disappears further. NPS market returns, by contrast, have averaged 10–12% per year in equity schemes over the past decade — though past performance doesn't guarantee future results.

GPF at Retirement: The Complication

GPF corpus at retirement is a one-time lump sum — entirely tax-free. But it's also finite. Once spent, it's gone. The defined pension continues for life (and to spouse). This is the key emotional and financial security argument for the old system — you cannot outlive your pension.

NPS, if you buy a good annuity plan, can also provide lifetime income. But annuity rates in India have historically been low, meaning you need a large corpus to generate a meaningful monthly income. For someone with 20–25 years of service remaining, NPS can plausibly build that corpus. For someone with only 10–12 years left, the corpus may be smaller and more vulnerable.

Our Honest Assessment

If you're a pre-2004 employee: your defined pension is a privilege that is increasingly rare globally. The GPF corpus is a bonus, not the main event. Maximise your GPF contribution, but your retirement security is already locked in via pension.

If you're a post-2004 employee under NPS: the 14% government contribution is genuinely generous. Invest in an equity-heavy scheme (Tier-I, Scheme E) in your early and mid-career years. Shift to G-Scheme closer to retirement. Check your NPS statement quarterly. The outcome depends heavily on choices you make — unlike your pre-2004 seniors whose outcome was fixed at joining.

Frequently Asked Questions

Can I contribute more than 10% to NPS voluntarily?

Yes. You can contribute additional amounts under NPS Tier-II or increase your Tier-I voluntary contribution above 10%. The additional voluntary contribution up to Rs. 50,000/year attracts a separate tax deduction under Section 80CCD(1B), over and above the Rs. 1.5 lakh 80C limit.

What happens to NPS corpus if I die before retirement?

The entire NPS corpus (both Tier-I and Tier-II) is paid to the nominee — no compulsory annuity purchase. There is no tax on the amount received by the nominee. This is an advantage over pension systems where survivor benefits are limited.