House Rent Allowance is one of the most tax-efficient components of a government employee's salary — but only if you understand the exemption rules. Many employees lose thousands of rupees annually by not optimising their HRA claim. This guide covers the city classification system, the three-rule exemption comparison, and real examples from common posting scenarios.

Important clarification: For Central Government employees, HRA is received as part of salary. The exemption rules under Section 10(13A) apply when computing how much of that HRA is tax-free. The two calculations — how much HRA you receive, and how much is exempt — are different and often confused.

How Much HRA Do You Receive?

The government pays HRA as a percentage of Basic Pay, determined by your city of posting:

- X Class Cities (27%): Delhi, Mumbai, Chennai, Kolkata, Hyderabad, Bengaluru, Ahmedabad

- Y Class Cities (18%): 13 state capitals + cities with population over 5 lakh per Census 2011

- Z Class Cities (9%): All other postings including most district headquarters

For a Level 7 employee with Basic Pay Rs. 47,600, this means Rs. 12,852 in X class, Rs. 8,568 in Y class, or Rs. 4,284 in Z class — per month.

The Three-Rule HRA Exemption Under Section 10(13A)

Once you know how much HRA you receive, the tax exemption is calculated as the minimum of three values:

- Actual HRA received from employer

- 50% of Basic Pay (for metro cities: Delhi, Mumbai, Chennai, Kolkata) OR 40% of Basic Pay (for all other cities)

- Actual rent paid minus 10% of Basic Pay

The lowest of these three is your tax-free HRA. The remainder is added to your taxable salary.

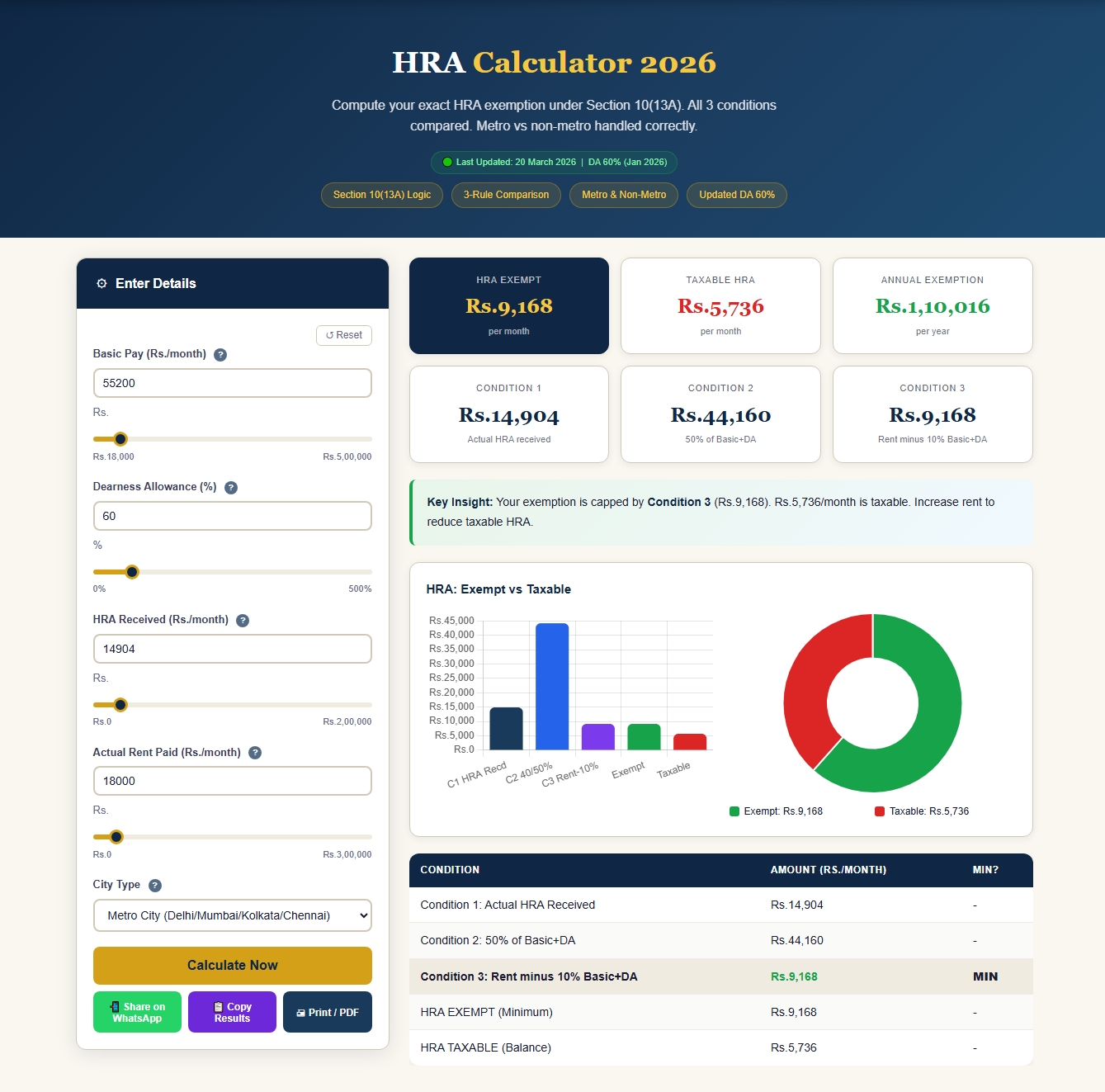

Real Example: X-Class City, Rented Accommodation

Take a Level 9 employee with Basic Pay Rs. 55,200, posted in Delhi (X Class), paying rent of Rs. 18,000/month.

| Rule | Calculation | Amount (Rs.) |

|---|---|---|

| Rule 1: Actual HRA received | 27% of 55,200 | 14,904 |

| Rule 2: 50% of Basic (metro) | 50% of 55,200 | 27,600 |

| Rule 3: Rent – 10% Basic | 18,000 – 5,520 | 12,480 |

| Exempt HRA (minimum) | 12,480 | |

| Taxable HRA | 14,904 – 12,480 | 2,424 |

So only Rs. 2,424/month of the Rs. 14,904 HRA received is taxable. The rest is fully exempt — saving approximately Rs. 750–1,500 in monthly TDS depending on your tax slab.

🏠 Calculate Your HRA Exemption

Enter your Basic Pay, city class, and rent paid to see all three rules calculated automatically with the optimal exemption amount.

The Z-Class Posting Problem

Employees posted in Z-class cities receive only 9% HRA — Rs. 4,284 for Basic Pay of Rs. 47,600. If they live in their own house or in government quarters, there's no rent paid and zero HRA exemption (Rule 3 becomes negative). In this case, the entire Rs. 4,284 is taxable income. It's a common situation in district postings and many employees don't realise this until they file their ITR.

Government Accommodation: No Exemption at All

If you are allotted government accommodation (government quarters, transit camp, or departmental housing), you do not receive HRA at all — the licence fee deducted from your salary covers the accommodation cost. In this case, no HRA exemption calculation is needed or applicable. Your gross salary is lower, but so is the deduction.

Living in a Different City Than Your Posting

A common scenario: posted in Bhopal (Y class), but family stays in Mumbai (X class), you pay rent in Mumbai. For HRA purposes, what matters is your city of posting — you receive 18% HRA (Y class rate). The exemption calculation uses 40% of Basic for Rule 2 (since your city of posting is not a metro), even though your family pays Mumbai rent. This is a situation where many employees over-claim exemptions incorrectly.

Documentation for HRA Exemption

Your DDO will ask for proof of rent payment before processing HRA exemption in Form 12BB. If annual rent exceeds Rs. 1 lakh, landlord's PAN is mandatory. Keep the following ready:

- Rent receipts for each month (signed by landlord)

- Rental agreement (for new or renewed tenancies)

- Landlord PAN card copy (if rent exceeds Rs. 1 lakh/year)

Frequently Asked Questions

Can I claim HRA exemption if I pay rent to my parents?

Yes — the Income Tax Act allows rent payments to parents. The parent must declare the rent received as income in their ITR. The arrangement should be genuine (actual bank transfer, not cash), and the parent should own the property. This is a perfectly legal tax planning method, not a loophole.

What if I'm in the New Tax Regime?

The new tax regime (default from FY 2024-25) does not allow HRA exemption under Section 10(13A). You receive the HRA as part of salary but the entire amount is taxable. For employees with high rent in metro cities, this is often the decisive factor in choosing the old regime — our Income Tax Calculator can show you the exact difference.

How is HRA treated after the 8th Pay Commission?

The 8th CPC is expected to revise HRA percentages upward as the DA has crossed 50%, which typically triggers a revision in city allowance rates. No official announcement has been made yet, but projections suggest X-class may rise to 30% and Y-class to 20% of Basic Pay.